Guest Contribution

Published in 3rd Quarter 2017

What is Takaful..? Explanation with Questions & Answers

By Mufti Basheer Ahmad

1. Is Risk Protection (insurance) against Tawakkul (total dependence upon Allah (SWT))?

No human actions change the Will of Allah (SWT) for our destiny. Whether a person has insurance/Takaful or not has no effect on future events. However, we are instructed to take precautions and then fully trust and depend upon Almighty Allah (SWT): In a Hadith narrated by Anas bin Malik, one day Prophet Muhammad (PBUH) noticed a Bedouin leaving his camel without tying it. He (PBUH) asked the Bedouin, “Why don’t you tie down your camel”? The Bedouin answered, “I put my trust in Allah (SWT)”. The Prophet (PBUH) then said, “Tie your camel first, then put your trust in Allah (SWT)”. [As quoted in Sunan At-Tirmidhi, 1981.]

2. Is all Risk Protection (insurance) Haraam (prohibited)?

The Fiqh Council of World Muslim League (1398/1978) resolution and The Fiqh Council of Organization of Islamic Conference (1405/1985) in Jeddah resolved that conventional insurance as presently practiced is Haraam, and that cooperative insurance (Takaful) is permissible and fully consistent with Shariah principles. Hence, conventional insurance is prohibited for Muslims (because it contains the elements of Riba, Al Maisir, and Al Gharar). By contrast, Takaful provides risk protection in accordance with Shariah based on the principles of Ta’awun (mutual assistance), brotherhood, piety and ethical operations.

3. What is Takaful?

Takaful comes from the Arabic root-word ‘kafala’ which means to guarantee, to help,to take care of each other’s needs. Takaful refers to mutual protection and joint guarantee. Operationally, Takaful refers to participants mutually contributing to the same fund with the purpose of having mutual indemnity in the case of peril or loss.

4. How is uncertainty (gharar) eliminated from Takaful contract?

Uncertainty can never be eliminated, it remains in the Takaful Contract as well. But, since the Takaful contract comes under Tabarru the uncertainty (gharar) is considered to be within tolerable limits under Shariah. Insurance, being a contract of exchange (muawadat), contains “excessive gharar” and is termed as fasid.

5. All Insurance is a form of Gambling or Wagering, which is forbidden in Islam.

Risk or uncertainty can be divided into: Pure Risk and Speculative Risk. Pure Risk involves the possibility of loss or no loss. For example, damage to property due to fire. Pure Risks are the subject of insurance risk protection and Takaful. On the other hand, Speculative Risk involves the possibility of loss, no loss or gain. For example, venturing into a new business, or gambling on horse race. Speculative Risks that include a potential Gain or Profit cannot be insured.

Takaful schemes use the principle of indemnification to compensate for the loss that occurs to a Takaful Participant. Takaful insures only Pure Risks and the claims are only payable in the event of Loss to cover repairs, damage, replacement of property, or an agreed fixed amount.

6. I don’t need insurance/Takaful.

A Takaful scheme gives us an opportunity to practice the virtues of Islam, including self-purification. Surah Al Maa’idah (V.2) says: “Help one another in furthering virtue and Taqwa (God-consciousness), and do not help one another in evil and transgression”. In a Hadith narrated by Ahmad and Abu Daud: Whosoever fulfills the intentions (needs) of his brother, Allah will fulfill his intentions. And Allah always helps those who help their brothers in need. The first Constitution in Medina (622 CE) arranged by Prophet Muhammed (PBUH) contained three aspects directly related to risk protection: social insurance for the Jews, Ansar and Christians; Article 3 concerning ‘wergild or ‘blood money’; and provision for Fidyah (ransom) and ‘aaqila. We should follow his (PBUH) example to meet our needs and social obligations.

7. Do Takaful contributions entail a higher rate than the conventional insurance premia?

No, Takaful companies are as competitive as their conventional insurance counterparts. Opting for Takaful will not make you pay the Cost of Being Muslim.

8. Can Takaful cover theft of my car?

Yes, Takaful companies offer the same variety of products offered by any insurance company, whether it is Fire, Marine, and Motor etc. In addition, we have the expertise and experience to deliver tailor-made specific solutions for the benefit and convenience of our clients. The only exceptions are those risks that are not in conformity with the Shariah, e.g. breweries, casinos etc.

9. How will I get a claim from a Takaful company?

All procedures, including claims, are the same as in conventional insurance companies. The difference lies in the nature of the contract, not in the procedures.

10. How is it ensured that all activities of Takaful companies are Shariah compliant?

All Takaful companies are governed by the “Takaful Rules – 2012” that require the Takaful operators to constitute a “Shariah Board” comprising of Shariah Scholars of repute.and a full time shariah compliance officer to ensure compliance of daily Takaful activities. Moreover, all Takaful companies have to undergo a “Shariah audit” as well, in addition to the customary Accounting audit, in each accounting period.

11. Is Takaful a modern day’s invention?

There are several examples in pre-Islamic history whereby families, tribes or related members throughout the Arabian Peninsula pooled their resources as a means to help the needy on a voluntary and gratuitous basis. Their practices were validated by the Prophet Muhammad (PBUH) and incorporated into the institutions of early Islamic state in Arabia around 650 C.E. So, the origin of Takaful dates back to the first Islamic community in Madina. Early precursors were developed in response to perils and risks associated with long-distance trade via caravans or sea voyage and included:

- Daman khatar al tarik (surety)

- Al – diyah and Al – aqila (wergild or blood money to rescue an accused involved in accidental killing).

- Fidyah (ransom of prisoners of war)

- Dawania – Mutual indemnification amongst officers working in the same department during the rule of the 2nd Caliph Umar Ibn Al Khattab.

12. Is Takaful transacted in other countries?

Takaful is a new phenomenon in Pakistan. The first Takaful company was established in 1979 – The Islamic Insurance Company of Sudan. Now, there are some 85+ Takaful Companies in over 20 countries. Takaful premium, currently around 0.1% (USD 3 Billion in 2004) of the Global insurance premium, is expected to increase to USD 12.5 Billion by the year 2015. The average growth rate of Takaful has been higher than that of the conventional insurance companies.

13. Are there any references in the Quran and Hadith in support of this Takaful concept?

Although Takaful has very old origins, the word Takaful is a modern day invention. You can find references regarding risk management and mutuality in Quran and Hadith: Takaful, the way it is transacted today, is based on the secondary source of Islamic Law Ijtihad.

14. How many Takaful models are there?

Alhamdolillah, in Islam there is room for diversity within certain prescribed parameters. Over the centuries, several Takaful Models have evolved which are approved by the Islamic scholars. While they all share the same fundamental goal of cooperative risk sharing, these models differ slightly in legal structure and organizational operations. Takaful Models are usually described by the Islamic contracts used; namely, Hibbah, or 100% Tabarru’ [Sudan], or Al Mudarabah [Bahrain/Malaysia], or Al Wakalah [Saudi Arabia], or Wakala/Waqf [Pakistan].

15. What Takaful Model is followed in Pakistan?

According to the Takaful Rules-2012, in Pakistan a Takaful product shall be based on the principle of Waqaf+Wakala+ Mudaraba modle. The relationship of the participants and the operator is directly with the WAQF fund. The operator is the ‘Wakeel’ of the fund and the participants pay contribution to the WAQF fund by way of Tabarru (contribution) .and Company receive defined wakalah fee as per rule 2012.

16. How does Riba exist in conventional insurance?

Riba exists in conventional insurance in following two forms:

Direct Riba – the excess on one side in the exchange between the amount of premium and the insured sum. Insurance is the sale of money for money, of a greater or lesser amount, with a delay in one of the payments.

Indirect Riba – the interest earned on interest-based investments. Riba exists in commercial insurance from the profits earned through investments of the premiums/funds in interest-bearing financial instruments such as stocks, bonds, and savings accounts, an unknown part of which is then used for the payment of claims to policy holders.

17. How is Takaful companies’ investment income Riba-free?

Unlike insurance companies, whose investment income may contain Riba, Takaful companies invest funds in Property, Islamic Banks, Shariah compliant Stocks and other Shariah approved securities like Sukuk bonds etc, with approval of their Shariah advisor.

18. Is Takaful just a change of label?

Although the end result is the same since both insurance and Takaful aim to provide compensation against possible losses, yet the crucial difference lies in the way that each does this. The notion “ends justify means” does not hold when it comes to Islam where both the ends as well as the means have to be in order. Chicken can either be slaughtered or given an electric shock; both achieve the same end, a dead chicken. However, the former way makes the meat Halaal for eating whereas the later renders it Haraam.

19. What advantages does Takaful offer?

- Wide product range.

- Competitive rates.

- Excellent client service.

- The unique option of “Surplus Sharing”.

- Above all, a way to help other Muslim brothers in need a deed whose reward has been promised by ALLAH.

20. What is meant by Surplus Sharing?

The Takaful Operator acts only as the Wakeel of the Waqf Fund. If, at the end of the year, there is surplus in the Fund (i.e. after adding all its income and deducting all the outgo), such surplus will be distributed amongst the participants proportionately after taking into account any claim benefits already availed.

21. Is there a single Participant Takaful Fund or separate PTFs for each class of business?

A General Takaful operator may create a single PTF or separate PTFs for different classes of business. But in Askari window Takaful practice of single PTF fund.

22. Will I be asked to pay more contribution in case there is a deficit in the PTF?

No. In case there is a deficit in the PTF, the same will be made good by way of interest-free loan “Qard-e-Hasna” from the Shareholders’ Fund (SHF). The Qard-e-Hasna will be paid back from the future surpluses of the PTF.

23. Is Takaful for Muslims only?

No, takaful is for all religious as Islam is a universal religion open to all. Likewise Takaful is open to all whether Muslims or non-Muslims. In Malaysia and Sri Lanka, even non-Muslims are opting for Takaful due to its commercial viability, greater transparency and ethical operations.

…………………………………………………………………………………………………………………………..

Published in 3rd Quarter 2017

Fire Insurance Policy Clauses (Part-9)

By Majid Khan Jadoon

Premium Payment Clause:

(i) By attachment of this Clause to the Fire Insurance Policy, it is thereby understood and agreed by the Insureds and the Insurers that the Insureds have under-taken the responsibility upon themselves that Premium of Risks Coverage Shall be paid to the Underwriters within the period of days, as agreed amongst themselves, after the inception of the Policy-period.

(ii) In case, however, if Payment of the Premium might not have made to the Insurers by the Insureds, within the mutually agreed and expressly Specified Period of days after the inception of the Policy, the Underwriters shall have the Right to cancel the relative Insurance Policy. However, the Insurers shall have to notify their decision to cancel the Policy, in writing, to the Insureds and any other interested Parties.

In such, a Scenario, the Insurers shall have to charge and be paid the amount of the Premium, on Pro-Rata basis, for the period they would have been on Risk.

However, it also must be born in mind that in case of a Loss or Occurrence that would have taken place prior to the Date of Termination of the Policy, giving rise to a Valid Claim, then the Insureds shall have to pay the full amount of the Policy Premium to the Insurers.

(iii) By this Endorsement, it is further agreed that the Insurers shall have to give Notice of Cancellation to the Insureds, as well as other relative Parties at least, 15-days prior to the Date of cancellation of the Policy which must be in writing.

In case, however, if the Due Premium would have been paid to the Insurers in full, prior to the expiry of the Notice Period, then the Notice of Cancellation would be deemed to have been revoked.

Conversely, it shall be considered that the Policy has been terminated at the end of the Notice period.

(iv) By Virtue of this Endorsement, it is also under-stood and agreed by Insureds and the Insurers that, in case of this Policy being on Co-Insurance basis, the Leading Co-Insurers, would be authorized to exercise all rights under this Clause of the Policy, as well as on behalf of all the Co-Insurers, pertaining to the same contract of Insurance.

(v) In case, any provisions of this Clause would have been found in-valid or un-enforceable by any Court of Administrative Body of Competent Jurisdiction, the invalidity or un-enforcibity would not affect other Provisions of this Clause which shall remain in full force and effect.

To be continued……

…………………………………………………………………………………………………………………………..

Published in 3rd Quarter 2017

Safety Tips

By Qayyum Pervez Malik

Safety

Recently on visiting CLPC website a very useful information regarding online safety tips, personal and family safety measures, educational institutions safety measures and safety measures on road while driving was found which should be publicized in the public interest to take benefit out of the remarkable contribution by CLPC so the same is being incorporated below with the courtesy of CLPC just to provide aid to CLPC in their efforts to save the public in general.

Online Safety Tips

Software

Keep your Antivirus updated, and use genuine software. Pirated software often contains malware (malicious software) that can compromise your computer and leave it open for someone to steal information.

Pictures

Avoid posting pictures of yourself, your family and your loved ones online. People with ill intent often manipulate these and may use them to blackmail you.

Passwords

Use strong passwords for your accounts (email, social media etc). Avoid using passwords that resemble words, birthdays, names of family members. The stronger your password they more difficult it is to break it. Your password should be a well maintained secret; do not disclose this to anyone. Young children must be taught to use passwords as and not to share them with friends.

Social Networking

If you use social media like facebook and twitter, set strong security settings. If you must share your pictures, don’t do it with strangers, or even friends of friends. Do not accept friend request on just looking the display picture & name of sender, verify the person before accepting the request.

Personal Information

Never give your personal information online (whether at home or at school) such as your name, home address, telephone, school name etc.

Parents

Keep a close watch on what your children do online. Your child must inform you who they communicate with online, and what they do. Look for signs that make your child look disturbed, uncomfortable or emotionally distressed. Remember anyone can be a victim of cyber bullying and blackmailing, even older children especially teenage girls. The internet is also a recruiting ground for criminals. Your child can easily get involved in the wrong company. You may install a Parental Control application on your PC/ Laptop/ Tablet for added safety.

Mobile phones/ Smart phones

Protect your phone with a password. In case it gets stolen the thief will have to wipe the phone’s data before using it. If your phone gets stolen, and there is no password on it, you may start getting obnoxious / blackmailing phone calls. Do not store personal information and photos on your phone unless it’s protected by a strong password.

Email Scams

Do not open email from just anyone. Also be wary of opening attachments. Be cautious of scams initiated by people claiming to be from companies like Microsoft, Google, and Facebook etc claiming that your account is being blocked unless you forward the email.

Lotteries and Inheritance

Remember you cannot win a lottery without buying a ticket. Do not reply to emails which claim that you have won a lottery in another country. Do not respond to emails from senders claiming to be for example wives, daughters or relatives of rich presidents with millions of dollars in their accounts. If you are conned into their trap, you will end up paying large amounts of money as “administrative fees”.

Online Jobs

Do not apply for online jobs without verifying the job site. There are fake companies who collect your personal data (picture, home address, email etc.) and can use your personal data for blackmailing.

Online Shopping

Verify the online shopping website before making any online purchase. Fake online vendors can collect your credit card details and other personal data.

Safety Measures Personal & Family

- Vary Your routes and timing when traveling to and from work etc.

- Use main routes and Avoid Badly Lit areas, Quiet residential / industrial / Barren areas and Single Lane roads

- Change your places of walking / jogging and vary timings

- Print only plain Visiting Cards

- Don’t talk on mobile phone while walking on the street or to your car even if you are inside your house/premises

- Keep a trained armed guard for protection

- Do not keep a fire arm unless you know how to use it

- Never give out any personal information, financial information or a credit card number during an unsolicited phone survey or sales promotion

- DO NOT carry your Debit/ATM/Credit cards in your valet unnecessarily

- Quickly see off your visitors and close the main gate

- If you receive “obscene” phone calls from strangers who ask questions regarding private matters, HANG UP!!!

- While you are away, criminals call at your home and attempt to extract personal information from your family members by introducing himself as your old friend/colleague and later on use this information to harass / threaten you. Please counsel your family members not to divulge any family information to unknown

- Be sure to keep a log of the dates and times of these phone calls

Chronic harassing / threatening phone calls should be reported to the Police or CPLC - Do not fall prey to the claim that “You’ve Won a Prize!” and all the caller needs is your credit card number

- Immediate Measures in case of Kidnaping for Ransom

- Inform Police / CPLC / Rangers immediately

- Family should be ready to be contacted via any medium by kidnappers.

- Never refuse to pay up, and never offer an initial amount till you have been properly guided by CPLC / Police / Rangers

- Preserve the evidence of contact:

- Phone number

- If Letter is received (DO NOT touch all over the letter, to save fingerprints. This will enable the authorities to conduct FORENSICS)

Safety Measures for Educational Institutions

Perimeter

- Construct High walls (10 feet minimum) with razor or electric protection

- Construct Elevated guard pickets

- Keep good visibility around perimeter

- Use Jumbo (FIBC) bags filled with sand

- Outer windows and doors should be secured with good quality key operated locks

- To reduce the casualties occurring due to flying glasses, all glasses should be protected with Blast Protection / Fragment Retention films

- Use physical barriers to prevent a hostile vehicle from driving into your premises

- Place physical barriers to keep all but authorized vehicles at a safe distance

- Make clear demarcation identifying the public and private areas of your premises

- Establish vehicle access control point at a distance from the protected site

- Construction should be a deterrence to scaling

- Do not allow any vehicle to park close to the gate

- Hawkers / Vendors should not be allowed near the premises

Entry & Exit

- Office / Institution’s Administration should have a control room at entry and exit points

- Develop tampered proof ID badges for staff to wear at all times

- Tampered proof entry passes should be developed for visitors entering into the premises

- Design visitors’ badges that look different from staffs’ badges

- Ensure that all visitors’ badges are collected when they leave

- No one should be allowed to enter without proper identification / verification

General Guidelines

- Install effective CCTV systems with backups at different locations

- Respective Departmental heads/Class Teachers should maintain family’s Network for effective Communication

- Any suspicious movement during or after office timings should be reported to the area police / CPLC

- Stagger Timings for different levels of students to minimize congestion

- Install Emergency Alarm Bell

- Perform regular patrolling by Armed Guards even outside school premises

- Assembly / Exit points should be identified for Emergency situations and be known to all staff and students

- All Staff members and senior students should be given Civil Defense training on regular intervals (Fire Fighting, First Aid, Building Evacuation, Lockdown etc.)

- Get Employees’ Verification from CPLC at the time of employment

- Ensure that your staff is security conscious

- Ensure that staff and students can identify and report suspicious activities

- Ensure availability of Safety procedures for use in emergency situations

In case of Terrorist Act

- Call 15 or CPLC emergency numbers 3566-2222/3568-3333 or relevant authorities and give them office/factory address

- Building Map should be ready for the Security Personnel

- Leave the bags and other belongings and rush to the emergency exit points

- No running on stairs (avoid Stampede). Avoid use of elevators

- Turn off all lights, fans, electrical appliances and equipment (Main Switch)

Suspicious Bag/Parcel Found

- Cordon off the suspected area and no one should be allowed inside the perimeter

- Do NOT Touch the Suspected Bag

- Call Bomb Disposal Squad

- Move everyone away to a safe location. Evacuate buildings

- Prevent others from approaching

- Communicate safely to staff, students, visitors and the public

- Use hand-held radios or mobile phones away from the immediate vicinity of a suspect item, remaining out of line of sight and behind hard cover

- Ensure that whoever found the item or witnessed the incident remains on hand to brief the police

Emergency Numbers

Display Emergency Contact Numbers at prominent places

Police Emergency 15

CPLC 3566-2222 / 3568-3333′ ‘111-222-345

Bomb Disposal Squad 15 or 99212667

Crime Control Cell Governor House ‘136’

Fire Brigade ’16’

Edhi Ambulance ‘115’

Safety Measures on Road / While Driving

- Install Alarm systems, Tracking systems, immobilizers in your vehicle

- Don’t talk on mobile phones while approaching your vehicle and while driving, or getting out

- Keep a distance from the vehicle in front in case you need to escape or make evasive maneuvers

- When approaching a parked car, kindly ensure that no suspicious persons are around

- Instruct drivers to park the car at a prominent place, lock it and stand away from the car while waiting for you to return

- In case someone blocks your road, try to choose an exit point even if it means damaging your car to escape the blockade

- Wherever possible, stay on the roads having fast moving traffic

- If someone forcibly enters your car, simply Bump into the car in front. This will create a commotion

- In case you have to ram a vehicle barricade, ensure you don’t damage the radiator of your car. Your angle of attack should be close to 45 degrees to the rear of the vehicle in front

- If suspicious vehicle follows you, honks or flashes its headlights from behind

- Stay calm

- Do not give way, speed ahead and alter your route

- Head for the nearest safe haven such as Police/Rangers post ,

- Military/ Navy barracks, Busy areas etc

- Try to lose them

- Never approach your house or your friends

- Watch your rearview mirror at all times

…………………………………………………………………………………………………………………………..

Published in 3rd Quarter 2017

Directors & Officers Liability – The Basics (Part-2)

By Ansa Azhar

In my previous article, I covered few basics on the D&O insurance with some of the concepts being.

- D&O Duties / risks / exposures

- D&O Insurance policy basic coverage / UW practice & considerations

This article will focus on,

1. Retroactive date / Claims made / Claims occurrence

2. Selecting the Limit of Liability

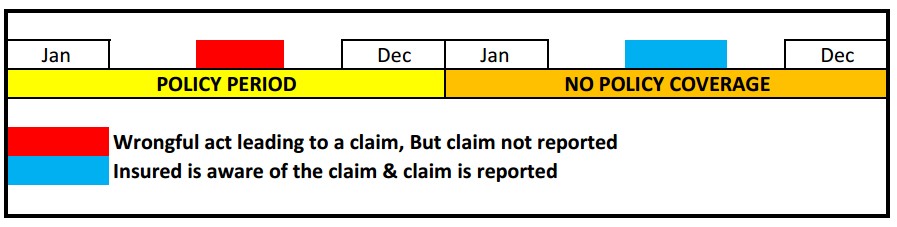

To understand retroactive date, let’s first look at understanding the how a claims made policy and a claims occurrence policy works.

Claims Occurrence Basis:

In a claims occurrence policy, the coverage is available for lifetime provided that the wrongful act has “OCCURRED”. As you can from the above Fig the wrongful act has occurred during the time when the policy was in force. However the claim is reported even after the policy expiry despite there is no continuity or a policy in force.

Claims Made Basis:

In a claims made policy, losses are covered provided that the claims are reported “WITHIN THE TIME FRAME OF THE POLICY”. Provided the claims are there is retroactive date in the policy. In most of the claims made policy forms a provision called extended period of reporting is made available to the insured (60-90) days after an expiry of policy, where losses if reported will be entertained. Any loss / claim reported beyond the extended period shall not be covered.

- Retroactive dates are basically enforced on claims made policies.

- These are given to companies who have been in business for a long time and have substantially exposure, however any pending or prior litigation are not entertained before the retroactive date.

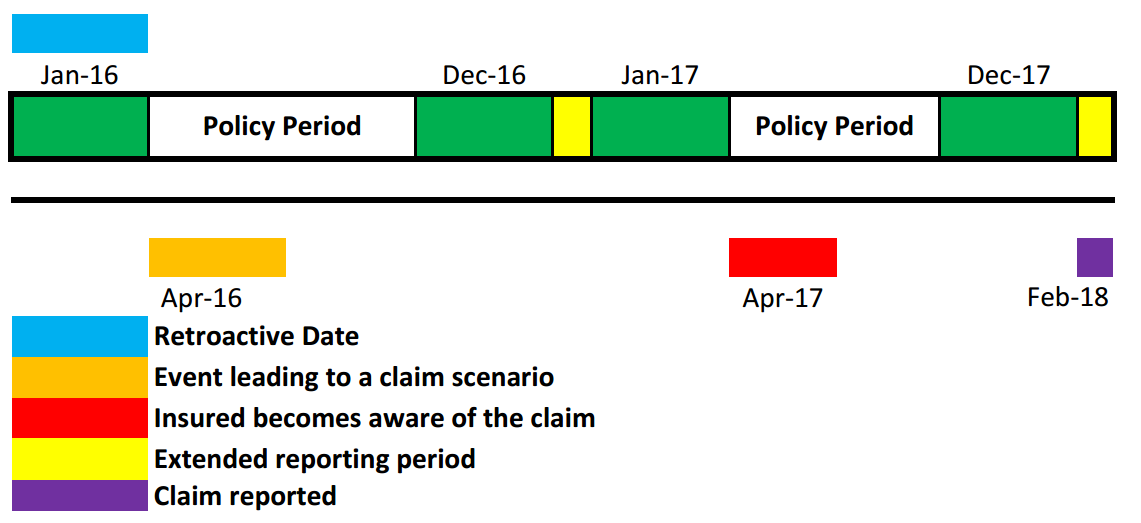

To understand how retroactive date functions – let’s take another example:

- Please note that the Original retroactive date is Jan-2016 – Claims made form

- In April 2016 there a event which is suspect to lead to a claim but the insured is not aware of that, Policy in renewed and continued for the next year

- In April 2017 the insured is aware of the claim and the claim is finally reported in Feb-2018 (During the Extended period). In this case the claims occur and fall after the retroactive period and are also reported when the policy is in force.

- Although the claims has occurred during the year 2016, due to availability of retroactive date provision, It provides the Insured with cover for claims arising from events that occurred before the start date of the policy (provided that the Insured did not already suspect there would be a claim).

Limit of Liability

One of the key challenges that many insured’s face is selecting the limit of liability. Selecting the limits depend on various important parameters with some of them being.

Organization Structure

- The structure of the organization plays a major role in determining the LOI, Both private companies and public companies are exposed to variety of risks based on their operating structure.

- A private company is controlled by a small group of investors or family members where there are only a limited number of stakeholders where a public company is exposed to huge risks are a portion of the company is being traded to the Public via IPO (Initial public offerings).

- Public company due their structure and a vast spread of stake holders are substantially exposed to risks than private companies thus requiring larger limits and also the severity of claims is higher in a public company.

Size of the Organization

The size of the organization is measured by some of the following factors:

- Annual revenue of the organization / turnover

- Market value of the organization

- Number of employees

The Executive risk of an organization is directly proportional to size and type of the organization:

- Larger the organization > Higher the exposure

- Smaller the organization < Minimal exposure

Number of Directors & Officers to be covered

The board of an organization can have:

- Chairman of the board

- Whole time & Full Time Directors

- Non-Independent directors

- Top Management / Key Executives

Not all of the executives require protection as some of the directors may not be concerned with have an executive protection for themselves however this completely depends on the organizations willingness and their risk management practices and hence LOI may be decided accordingly.

Geographical Operation

Geographical operation plays a very important role in selecting the LOI, as some of the countries may be based on one country and their revenue and list of clients could be from a different continent. Each country has its own set of laws governing the duties of the directors and officers:

United States

- The Dodd-Frank Wall Street Reform and consumer protection act 2010. It focuses on Financial stability regulations and GAAP ( general accepted accounting principles ) to ensure transparency in financial dealings

- The Sarbanes Oxley act which focuses on standards and requirements for public limited companies

- The Securities exchange act of 1934 which is law which governs on stock trading and operation of financial markets

India

- The Companies Act 2013(1956 originally) amended in 2013, which regulates the company, Duties of directors and officers, their responsibilities and accountability. This act also has provision for corporate governance and accounting and financial reporting standards.

- The SEBI (Securities and exchange board of India) Act 1992 which is regulator for stocks and securities market in India.

Bench marking with Peer organization

One of the most standard methods of selecting LOI is by bench-marking with peer organizations. Where UW and Brokers play a very vital roles as they have experience of writing and rating risks with similar risk exposures.

Claims Trend & Budgets

- Claims trend is a very important factor in deciding the LOI, they are based on all the above factors mentioned below including the one mentioned in my previous post Common Losses from D&O exposures.

- At the end of the day it all boils down to one key-important factor, Yes THE BUDGET! Are clients willing to pay for the risk exposure they seek cover to? Coverage is readily available in the market; But the Expense and the cost are always considered as important factors for selecting LOI.

…………………………………………………………………………………………………………………………..

Published in 3rd Quarter 2017

Reinsurance and its Benefits

By Nasir Siddique

What is Reinsurance?

We have seen how normal insurance companies work. They pool a large number of people sharing a common risk i.e. risk pooling. But it is interesting to know that even the insurance companies that sell you insurance buy an insurance. These insurance companies buy insurance to make sure that they are able to fulfil the obligations they have towards the customers. This process of an insurance company transferring their risk to another insurance company is called Reinsurance.

The company that transfers the risk is called the ceding company and the accepting company is called reinsurer. The reinsurer agrees to indemnify the cedent against complete or a part of a loss which the primary insurance company may bear under certain insurance policies that it has sold. In return, the cedent pays a premium to the reinsurer. Also, the ceding company discloses all the information needed by the reinsurer to assess, set price, and manage the risks covered under the reinsurance contract.

Let’s give you an example:

Mr. Naveed has a life insurance policy with an insurance company State Life 10 crore. The insurance company now wants to transfer, say 30% of the risk, to the reinsurer. Then, in the case of loss the ceding company now has to pay the whole sum assured to Mr. Naveed beneficiary and ask the 30% it earlier insured from the reinsurance company. Mr. Naveed or his beneficiary has Naveed and the primary insurance company and thus, the company is bound to settle the complete claim asked by Mr. Naveed or the beneficiary. The contract between the ceding company and reinsuring company is separate.

Who offers Reinsurance?

It is important to note that not all insurance companies that are in the business play reinsurer to other insurance companies. The capital requirement to settle the ceding company’s claim is much higher.

Who buys Reinsurance?

We already know that primary insurance companies need reinsurance. But there are companies who specifically buy insurance to keep the business running. The reinsurers deal with the ceding companies, reinsurance intermediaries, multinational corporations and banks.

The business model of the primary insurance company decides how much of the business needs to be insured. The company also considers its capital muscle, risk appetite, and assess the current market conditions before buying the reinsurance.

Insurers whose portfolios are vastly exposed to natural or catastrophic disasters like flood, earthquakes, etc. need insurance cover the most. While small players that might need a bigger reinsurance cover because of the diversity of insurance risk coverage and large client base.

Companies with a focused line of working or with a specific clientele need more reinsurance cover than those with a diverse range of clientele. In the case of commercial portfolios, even though the risk number is small (aviation industry or utility industry) the exposure is very large and thus such companies need more reinsurance cover.

In many cases, companies seek the insurance cover in order to benefit from the reinsuring company’s expertise and financing while the ceding company expands its product range or move into a new geographical area.

Types of Reinsurance:

There are two types Reinsurance:

1. Facultative Reinsurance:

Facultative reinsurance is the type of reinsurance which covers a single risk. It is considered to be more transaction-based. Facultative reinsurance allows the reinsurer to assess the individual risk and take a call on whether to accept or reject it. The profit structure of the reinsuring company plays a part in deciding which risk to take. In such agreements, the ceding company and the reinsurer create a facultative certificate that states the reinsurer is accepting a specific risk. This type of reinsurance can be more expensive for the primary insurance companies.

2. Reinsurance Treaty:

In this type, the reinsurer agrees to accept all of a specific type of risk from the primary insurance company. In treaty contract, the reinsuring company are bound to accept all the risks that are mentioned in the contract. There are two types of the treaty contract:

Quota or Quota Share: It is the consolidated type of risk-sharing The ceding company transfers some percentage of the risk to the reinsurer and keeps a certain percentage to itself. The percentage in fixed in the given contract.

Surplus Insurance: There are three aspects to look at:

1. What is the maximum cover the reinsuring company is ready to accept?

2. What is the maximum loss (sum assured for Life Insurance and indemnity assessed for General Insurance)?

3. What is the percentage of risk to be transferred?

After calculating these factors, the treaty contract is proposed.

How Risks are Covered?

There are two ways in which reinsurer covers the risk in the given contract:

1. Risk of Excess Loss:

The reinsurer proposes to give a certain amount as a cover to the ceding company if the loss occurs up to a specified amount. For eg. The reinsurance company agrees to pay PKR 50,000 for a loss in excess of PKR 1,00,000.

2. Aggregate Risk Excess of Loss:

It is similar to the above-mentioned But here, the primary insurance company has to wait for all the claims in a year, sum all of it and if the calculation exceeds the cover promised by the reinsurer, then the promised amount will be covered.

Premiums in Reinsurance:

There are again two types of paying a premium:

Original Premium or Direct Premium:

If say 30% of the risk is transferred to the reinsurer then 30% of the premium received by the primary insurance company is directly transferred to the reinsurer.

Revised Risk Premium:

The reinsuring company doesn’t care what the ceding company charges their client for premium. It states its own premium to the cedent for a certain risk to be covered.

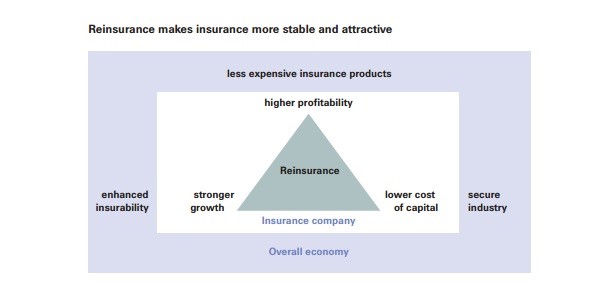

Benefits of Reinsurance:

- Reduce the volatility of results of underwriting.

- There is a flexibility in financing and there is also a capital relief.

- The ceding company can access the reinsuring company’s expertise and services especially in the fields of pricing, underwriting, product development, and claims

Reinsurance boosts Insurance Business

The major advantage of reinsurance is that it assists in the boom of insurance business. It enables every insurer to accept insurance business as the total risk will be distributed among other reinsurers.

If there is no reinsurance, the insurer may not be willing to take up risks, particularly when the risk exceeds beyond his capacity to manage.

Reinsurance reduces the risks

The prime principle of insurance is to reduce risk. As the risks are spread across wider area, the loss of the individual is minimized which gives the insurer the secured feel. The revenue of insurance companies are stable due to reinsurance. It also helps the insurance companies to gain knowledge about various types of risks and the basis of rating the risks in the future.

Reinsurance Increases Goodwill of Insurer

Reinsurance helps to boost the overall confidence and goodwill of insurer.

When the insurer develops confidence, he understands the nature of risks involved beyond his capacity.

Reinsurance motivates the insurers to undertake and spread the risks. Hence the liability of insurer is limited to the maximum.

Reinsurance Stabilizes premium Rates

The premium rates of insurance are stabilized by reinsurance. Generally, the premium rates are calculated on the basis of the loss experienced by the insurer in the past, due to the risk concerned. Reinsurance takes into account of all these data and fixes the premium rate according for various types of risks under mutual agreement.

Thus reinsurance stabilizes the fluctuations in the premium rates of various types of risks.

Reinsurance Protects the Insurance Funds

The insurance funds of the insurer is well protected due to reinsurance. Additional security and peace of mind is an added advantage of reinsurance for the insurer and the company that offers the insurance.

Reinsurance Reduces Competition

The competitions between inter company is reduced as everyone work in a cooperative manner and with the helping tendency in the insurance business. Thus reinsurance helps to control competition and increase overall morale of the employees in the insurance business.

Reinsurance Reduces profit fluctuations

The reinsurance plans reduce, to a considerable extent the violent fluctuations in the profits of the company. If on the other hand, heavy risks are retained by the original insurer, his profits are greatly upset due to a heavy single loss.

Reinsurance Encourages new enterprises

It encourages the new underwriters, who in their early period of development, have limited retentive capacity. In the absence of reinsurance facility, the tremendous growth of new enterprises is doubtful.

Reinsurance Minimizes dealings

Due to the reinsurance scheme, the insurer is required to indulge in the minimum dealings with only one insurer. In the absence of insurance facility, the insured will have to approach several insurers to enter into various individual insurance agreement on the same property. This involves considerable cost, loss of valuable time and slower down the pace of protection cover.

These benefits are applicable for both Life and Non-Life Insurance. However, due to different approaches of the primary insurance companies, the importance of these benefits may vary to different sectors.

Conclusion:

Reinsurance is one of the major capital and risk management tools available to the primary insurance industry. But it is rarely heard outside the insurance sector. Even the reinsuring companies have their own reinsurers called Retroinsurers. Reinsurers provide protection to the insurance industry for a diverse range of risks and also gives them a capital relief. Reinsurance makes insurance sector more stable and attractive.

…………………………………………………………………………………………………………………………..

Published in 3rd Quarter 2017

Branding Yourself!

By Ayesha Aslam

Personal branding is about managing your name — even if you don’t own a business—in a world of misinformation, disinformation, and semi-permanent Google records.

– Tim Ferriss

Your personal brand is a voice or theme that articulates what makes you different or unique. Your brand helps to express your unique value to an employer, and differentiates your skills, experiences, and abilities from your competition. A successful brand should be unique, credible, consistent, and relevant. Personal branding is an important part of the job / internship search, because of the competitiveness of the job market. It also improves your likelihood of finding a good fit within a company and gives you increased self-confidence and focus in your search.

Confidence (or the lack thereof) is another big concern with personal branding. Simply put, if you are not confident in yourself or your work, you will have a lot of trouble branding yourself. There are many ways to build your self-confidence, but what it usually comes down to is improving yourself, constantly and laboriously.

When Should You Start Branding Yourself?

Today, right now, is the very best time to start working on your personal brand. Whether you realize it or not, you probably already have the beginnings of a personal brand that you’ve been building up since you began your professional career (or very likely, even before that). Whether you want to continue in this direction or strike out with a whole new brand, the sooner you get started pushing that brand the direction you want it to go, the sooner your brand will be strong enough to help you get where you want to be professionally.

Why you need Personal Brand:

There are many reasons you should want to develop a personal brand.

Building a positive reputation (whatever that might mean in your field) can lead to increased word-of-mouth advertising for you and your services. When your reputation spreads and precedes you, it also makes interactions with potential clients that much easier, allowing you to spend less time convincing them to hire you, and more time negotiating the scope of services and payment (and actually working on the project).

Managing a personal brand helps you build a kind of brand equity, which will grant your name and products a certain star power. The more you refine your brand, the more targeted your message becomes and the more you will be doing the work you want to do, with the people you want to be working with, and at a price point that everyone can agree on.

And those are just the short-term benefits! In the long run, taking the time to filter out the rough and think through what kind of professional you want to be and how you want the rest of the world to see you can actually make you a much more skilled, fulfilled and happy person.

Labelling Theory:

This theory is based on the premise that an individual’s identity is partially (or largely, depending on who you talk to) determined by the words that are used to describe them. According to this theory, if a child is told they are bad over and over, they will end up being a bad person. On the other hand, someone who is told they are good-looking or intelligent will have a more positive self-image. This theory illustrates why it is so important to use the correct words when describing yourself, your work and everything related to your personal branding.

Labels are powerful and, therefore, you should refer to yourself, even if just in your own mind, as the title you wish to achieve. You shouldn’t lie about it (introducing yourself as a Nobel Prize winner if you haven’t won one yet, or a doctor if someone is injured in an accident, for example, would be a bad idea), but always make sure you are preparing yourself for where you want to be, not where you are.

Your Skill Set:

No matter how great your branding is, at some point you will need to have a skill (or ideally, several). In fact, a big part of building your brand is dependent on your current and future skill sets, how you develop them, and how you use them once you’ve got them. A skill set is a group of related skills that, when put together, add up to a marketable package. For example, an underwriter might have one skill set if he is good with MS excel and internal software. But being proficient in different communication styles is different set.

It is important, from a self-marketing standpoint, to develop a handful of well-developed skill sets if you want to be truly successful. Even those professionals that focus on one aspect of their craft in order to become the absolute best at what they do require supplementary skill sets. In fact, I would argue that it’s nearly impossible to become really great at anything without a supporting cast of skill sets to keep you moving forward and to give you a grasp of the big picture.

So the first step in expanding your arsenal of skills is to figure out what skill sets you already possess. Whether your list is massive or miniscule, I guarantee you have at least a few well-developed skill sets. Once you’ve determined what you already CAN do, it’s time to figure out what you’d like to be able to do. This doesn’t have to be at all related to what you already can do: having links between what you do now and what you’d like to do helps, but is not necessary. Now, go through and find points of overlap and bring it in action.

The Company You Keep:

There is something to be said for hanging out with the right crowd. Where personal branding is concerned, there are two main types of ‘right crowd’ that you will want to be associated with, and a whole host of other crowds you probably don’t want to be. The good crowds may already exist or they may not. Either way, having the support of the right crowd (or two)(or three) is important in the development of your personal brand.

The first crowd you will want to find or build is your core support group. This crowd consists of people who you know you can trust with anything, even if their professional goals do not align with your own. The largest investment you will make in maintaining a healthy core crowd is the energy it takes to be a friend back to them.

Work hard to be a good friend to others, and you will usually be rewarded in kind. If that doesn’t work, find a new group of people, because you shouldn’t be wasting your effort on deadwood.

The second crowd you will want to have is your collection of professional friends and colleagues. These people are perhaps not as close on a personal level as your first crowd, but they know your business inside and out, and you know theirs. You all lean against each other, but also maintain certain barriers, keeping the relationship mostly professional in nature; if your core crowd invites you to birthday parties, this crowd invites you to lunch meetings. It’s important to have this group to back you up when you need a recommendation, new connection or advice on a tactical business decision.

Working on your personal brand:

As with many other worthy undertakings, the first steps in developing a personal brand are the most difficult, and where many people decide that it’s too much for them. This is not because it’s tedious or cumbersome or at all skill-intensive, but rather because it involves looking at yourself and your attributes in a brutally honest way. It takes guts to unflinchingly take stock of the details of your life, personality and achievements.

This, of course, may not be much of a chore for the rare few that have a natural self-confidence and can joyously look in the mirror, like what they see, and decide to improve it further. For the rest of us, however, it can be a very eye-opening and sometimes soul-searching activity, which forces us to take stock of our weaknesses even while celebrating our strengths, which can be a real blow to the ego.

Make two columns on a sheet of paper, and in the first column list ten things that you think people really like about you. Anything is game, from your winning smile to your cunning jokes to your honest demeanor. It can be about you as a person (you always know the latest sports scores) or it can be about you as a businessperson. Be honest with yourself; at this point we are looking at what is currently there, not where we want things to be. Ask friends, family or clients if you don’t know, as most will be happy to help and will be able to offer a less-biased opinion on the subject.

In the second column, write down ten things that you think you could improve upon. Again, this list can consist of things about you personally (you have a bad habit of telling jokes that make people uncomfortable) or professionally (you’re always at least a few minutes late to meetings). With this one it will be very important to ask others, and to unflinchingly accept their answers. Part of self-improvement is being able to accept criticism constructively, so tell them about what you’re working on, tell them to be honest, and then write down what needs some work.

Take a look at the sheet of paper with the two lists; this is the foundation of your personal brand right now, at this moment. The trick to developing and strengthening this foundation is to emphasize certain aspects from the first column, while decreasing or completely eliminating lines from the second column.

Communication Habits:

Developing a robust brand is one thing; deploying it effectively is quite another. The challenge is to be able to do both successfully. Deployment is how well you communicate your brand.

Some mediums that are used for brand communication are:

Email:

Electronic mail is usually considered a tool of extremely simple communication channel most people have come to expect. Even within those boundaries, however, there is room to make your mark. Many people choose to style their signature in such a way that it is clear who they are, what they do, where they do it and how they can be reached. This can be taken a step further with a nicely formatted chunk of text containing the information that’s on your business card for your signature.

Phone:

Telephonic conversations is a medium to pass your brand image through ears to brain. How do you answer your phone and the courtesy offered by your tone all endorse your brand.

Texting:

Use of text services aren’t advised for professional matters, however, if you have to then the language and punctuation should be appropriate.

Final Words:

Your visibility to your network, the uniqueness you offer through your skill sets, credibility and value you offer along with the emotional connection makes up your brand. However, consistency is the heart of designing or re-designing your brand. You have got to be rock solid in terms of getting your brand message out in a consistent manner.

Zinger capture an equation to describe what a personal branding is:

Personal Brand = (Strength + Value + Visibility) x Engagement

Here is what it implicates:

- Each attribute alone is insufficient to sustain a brand.

- A brand cannot be sustained by having just one or two of these attributes; all three are necessary.

- But even all three attributes combined are still insufficient to sustain a brand if there is minimal or no engagement with each over time.

Personal branding or rebranding is not something that you can invest an hour or two in and then never have to think about again. It’s a 24/7, full-time job that takes a lot of attention, tenacity, and cajones to do right. Fortunately, once you get into the habit, it’s something that can fit seamlessly into your life without having to keep it at the forefront of your mind.

“All of us need to understand the importance of branding. We are CEOs of our own companies: Me Inc. To be in business today, our most important job is to be head marketer for the brand called You.”

– Tom Peters in Fast Company